Ok, now what?

The world was coming to an end

For those of us in the collections and ARM industries, Covid had seismic and permanent impacts covered amply elsewhere. It is rare to have an entire business model come under immediate and intense stress (“10 years of change in 8 weeks”), and it was equally remarkable how the industry emerged through the crucible with rapid business model changes. Amazingly, the industry pivoted deftly and continued to operate with strong success.

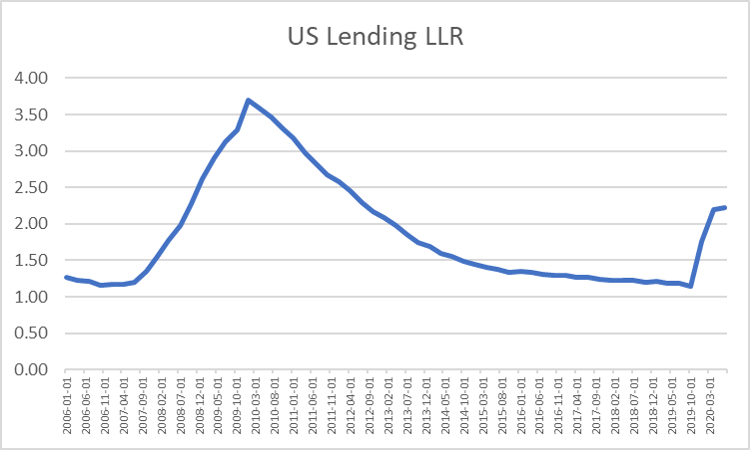

It was also stunning how rapidly loan loss reserves were built. In the 3 quarters from 4Q 2019 through 2Q 2020 industry reserves more than doubled, and in that time went from a generational low (1.15% in 3Q 2019) climbing to nearly 60% of the 2008 recession peak by mid-2020. That is a tremendous amount of velocity for a “resilient” industry. Many of the brightest minds in the industry began forecasting loss experiences in line with, or worse than, the 2007-08 crisis. The world of credit seemed headed for some very dark days.

Until it didn’t… and the world turned upside down

We all know what actually happened.

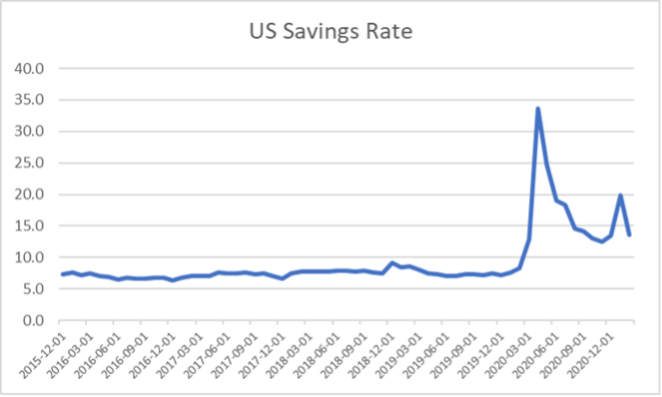

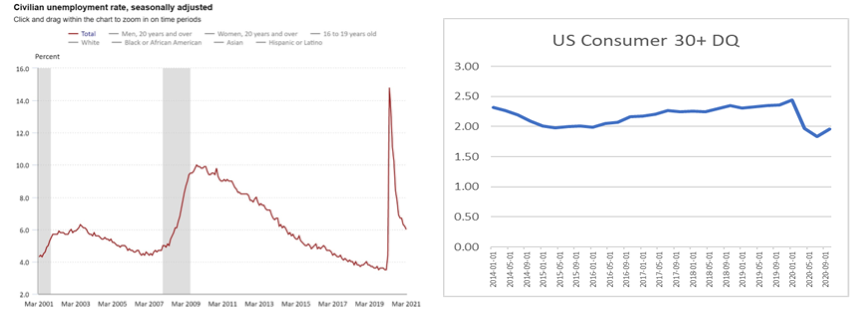

Massive government stimulus, combined with aggressive forbearance programs by lenders, was effective at muting the catastrophic impacts of the pandemic. In fact, despite huge increases in unemployment and a global pandemic, US consumers actually increase their savings which also cause consumer delinquencies to drop by almost half from already historically low levels!

Which brings us to recent earnings reports for 1Q 2021. Banks are reporting huge profits driven, in part, by massive release of built-up loan loss reserves. The industry is very healthy, as shown above. It would appear, then, that the credit crisis has perhaps passed and the industry can revert to a pre-pandemic footing.

Macro trends

Against the backdrop of a dramatically improving credit environment, three macro trends will still drive transformative change in the collections industry:

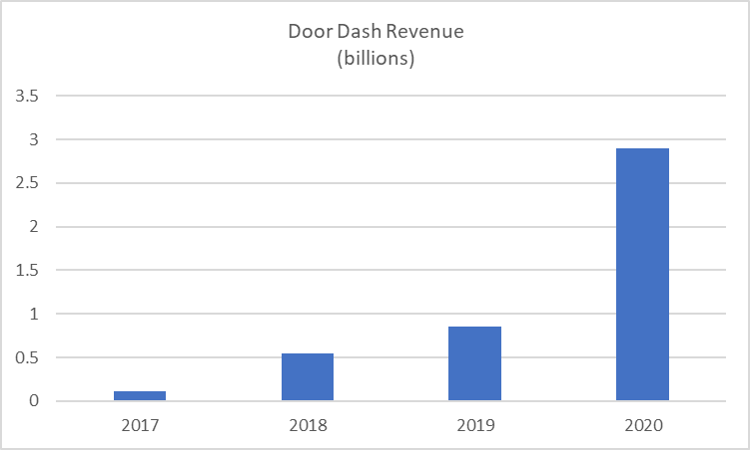

- Consumer omnichannel expectations (accelerating): Consider Door Dash, they were already a successful company back in 2017 helping drive massive consumer behavior around food delivery, and yet their revenues grew have grown 26x since 2017. “Traditional” thinking does capture the underlying power of these types of shifts which are increasingly common and were amplified by Covid.

In thinking about collections activity, consumers have had an extraordinary twelve-month period to re-evaluate everything and adopt new practices. The expectation for all-digital, highly customized experiences is now unmistakable, any lender standing still has actually lost substantial ground.

A recent McKinsey research article noted “companies are three times likelier than they were before the crisis to conduct at least 80 percent of their customer interactions digitally.” Back in the old days landline revenue was great for telephone companies, until it vaporized and gave way to wireless. Similar dynamics are at play in collections, where there remains an extraordinary reliance on call center operations and telephony infrastructure to achieve business objectives despite overwhelming long-term evidence that effectiveness of the outbound dialer continues to erode.

- Technology transformation and obsolescence (accelerating): The credit and collections industry is experiencing the double headwind of catching up from a period of delayed investment (roughly, 2009-2020) as well as accelerating technology innovation looking to reshape the industry model.

With a best-in-a-generation economy coming off of the 2007-08 recession, the industry shifted investment to revenue growth and allowed collections technology to stagnate, causing a significant pivot in 2020 when Covid arrived. Further, there has been an amazing array of technologies brought to market in the past few years to attack a dated infrastructure ripe for innovation.

Collections activity still relies heavily on a call center agent model, which is costly and increasingly and persistently less effective over time. Whereas technology literally transforms industries, the underlying structure of collections has in fundamental respects not changed much at all.

- A transformative regulatory framework (CFPB Reg F) comes online early 2022 after a slight delay (emerging): While much of the industry is talking a lot about Reg F, many have not yet formed specific action plans.

The remainder of 2021 provides a valuable window of opportunity to form concrete plans and to prepare adequately for the anticipated regulatory framework commencing in 2022. Not only are market forces driving change, but the main regulator is unambiguously signposting its expectations for an overhaul of collections activity in the not-distant future.

What Next?

“Your business might not be omnichannel, but your customers are.” – “Boosting your business growth with omnichannel communications while creating happy customers”, Wall Street Journal

Collections strategy and operational effectiveness is and has always been about the Reach (the ability to contact delinquent customers), Conversion (the ability to generate a payment or a promise from a right party contact), and Yield (the amount of the payment).

The persistent and continued reduction over time of the ability to contact customers (reduced Reach percentage) is a permanent headwind that is much more impactful than any great operational practices and techniques available to a highly skilled collector. If you cannot engage or talk to the customer, you do not collect payments.

The only option, then, is to offset the loss of telephony contact rates with non-phone outreach, which by now is table stakes. The ability to truly drive omnichannel execution, which is orchestration and synchronization over time and across channels, remains a significant opportunity. Additionally, enabling customer feedback loops within the operating environment to continuously optimize contacts strategy.

If your customers show you that they prefer digital banking on Tuesday mornings and that they are responsive to text messaging, you should be able to leverage that data either real-time or within very short windows. This is machine learning, and it is not difficult to access and use.

Customer feedback is clear – they will not answer an incoming call from any source not considered trusted. And commonly available technology (call blocking) provides ample power to permanently block the caller.

The combined impacts of radically changed consumer expectations, the availability of new technologies to drive engagement and efficient collections as well as the soon-to-be acceleration of regulatory change cannot be overstated.

Consumers will always prioritize debts for repayment based on kitchen-table factors such as how well they are treated or how personalized the experience is during a stressful and challenging time. As more lenders invest in creating state-of-the-art technologies to support 21st century collections, it is increasingly critical for lenders to invest in forward-oriented collections technology.

That said, the process of selecting the right collections technology can be a time-consuming and resource-intensive process that requires alignment across an organization. We agree with and follow our partners at Bridgeforce who have designed a timely and useful 3-part webinar series on vendor selection, intended to help companies assess digital readiness, navigate the challenging process of selecting the right vendor and prepare for a successful implementation. If you haven’t already, now is the time to pursue a digitized collection strategy that helps you solve for today and prepare for tomorrow.

=

Ray Peloso, Chief Customer Officer at Finvi, brings 25 years of diverse consumer lending experience, having held executive leadership roles at Royal Bank of Scotland, Capital One, Citibank, MBNA and Katabat. Ray’s prior expertise in consumer credit and lending underpins a clear vision and understanding of the challenges faced by our clients in today’s rapidly evolving digital economy.

More from Ray Peloso